Everything You Need to Getting Started in Canada

Our Welcome to Canada Bundle has been designed to include all the basics of what you will need to establish your finances in Canada. Below is a summary of what is included:

WELCOME TO CANADA BUNDLE

- An Introductory Guide to Finances in Canada

Credit Builder Program:

- Cash secured loan - term between 12 and 60 months

- No application fee.

- Interest rate on the loan would be Compass Credit Union Prime.

- Loan money held in a Term Deposit.

Chequing Accounts features:

- Eligibility: Must have arrived in and be living in Canada within the last 3 years.

- No Monthly Fees – (for the first two years - $17.95 / month after)

- Unlimited POS transactions

- Unlimited cheque/preauthorized debits

- 5 Free E-transfers

- Free personal cheques

- No interest

Savings Account – Plan 24

Collabria Credit Card (subject to approval under the New to Canada Offer)

Introductory Guide to Finances in Canada

Mortgages (Buying a Home)

Buying a home in Manitoba is very achievable for immigrants and newcomers to Canada, even if you are new to the financial system. The key is understanding what lenders look for and what options are available to you.

Credit Score: What’s Required?

Your credit score (see in depth explanation on Pages 4 & 5) helps lenders decide if you qualify for a mortgage. A score of 650 or higher is typically preferred. Newcomers, however, often have little or no Canadian credit history, making getting a mortgage a bit more challenging.

It is, however, also possible to prove creditworthiness

through:

- Proof of rent payments

- Bank statements and savings history

- Proof of consistent payments for utilities, cable,

childcare expenses, and insurance premiums

If satisfactory creditworthiness still can’t be established, then it is still possible to get a mortgage if you have a co-signer / guarantor.

Down Payment: How Much Do You Need?

In Canada, the minimum down payment depends on the home price:

5% for most homes under a set value

10–20% or more may be required if:

- You have limited credit history

- You are using a newcomer mortgage program

- The price of the home is above $500,000

Your down payment must come from verified funds, such as savings, gifts from immediate family, or funds transferred from abroad (with proper documentation).

Additional Costs to Budget For

Besides the purchase price, plan for:

- Legal fees

- Home inspection fees

- Property taxes

- Home insurance

- Moving and utility setup costs

These costs should be part of your overall savings plan.

Get Pre-approved

Getting pre-approved before you shop for a home lets you know what you can afford. You can get pre-approved for either personal or joint mortgages. To get pre-approved you will need important documents such as:

- Current pay stub

- Most recent T4

- ID

- Confirmation of down payment funds

- A list of assets and liabilities (including: investments, vehicles, credit cards, loans, or any other financial obligations.)

For more information, pre-approvals, or to apply for a mortgage, book an appointment to speak with one of our loans specialists:

Ways to Save

Tax‑Free Savings Account (TFSA)

- Best for short‑ or medium‐term goals

- Money grows tax‑free, and withdrawals are not taxed

- Flexible options

- Ideal for students and newcomers just starting to save

First Home Savings Account (FHSA)

A First Home Savings Account (FHSA) is a registered savings account designed to help Canadians save for their first home. It combines features of both a TFSA and an RRSP.

- Contributions may be tax‑deductible, like an RRSP

- Money grows tax‑free, and withdrawals are tax‑free when used to buy a qualifying first home

- Funds can be used for a down payment or other eligible home‑buying costs

- If you don’t end up buying a home, unused savings can usually be transferred into an RRSP without immediate tax implications

The FHSA is ideal for first‑time buyers who are planning ahead and want to maximize tax advantages while saving for a home. (Must be a permanent resident to qualify for this account)

Registered Retirement Savings Plan (RRSP)

- Best for long‑term retirement savings

- Contributions can reduce your taxable income

- Withdrawals are taxed

- More useful once you’re earning a steady income

Many people start with a TFSA first, then add an RRSP as their income grows.

Registered Education Savings Plan (RESP)

A Registered Education Savings Plan (RESP) helps families save for a child’s post‑secondary education, such as college, university, or trade school.

- Anyone can open an RESP for a child (parents, grandparents, guardians)

- Contributions grow tax‑deferred

- The Canadian government may add education grants to boost savings

- When the student uses the money for school, withdrawals are usually taxed at the student’s lower tax rate

RESPs can help reduce the financial burden of education by starting early and taking advantage of government incentives.

For more information on our investment products and for investing advice, speak with one of our investment specialists:

What Surprises Newcomers the Most

How Canadian Finances Differ from Other Countries

Canada’s financial system is often described as stable, conservative, and highly regulated, but it can feel quite different for people arriving from other parts of the world. Here’s what stands out most.

How Credit Scores Work in Canada

What Is a Credit Score?

A credit score is a three‑digit number that represents how reliably you use borrowed money. In Canada, credit scores generally range from 300 to 900, with a higher score indicating lower risk to lenders.

Your credit score is calculated using information from your credit report, which is maintained by Canada’s two main credit bureaus:

- Equifax Canada

- TransUnion Canada

These bureaus collect information from banks, credit unions, credit card companies, and lenders, then use scoring models to estimate how likely you are to repay credit on time.

What Is a Credit Score Used For?

In Canada, credit scores are widely used to make financial and lifestyle decisions, including:

- Approving credit cards, loans, and lines of credit

- Mortgage approvals and interest rates

- Renting an apartment

- Setting utility or phone service deposits

- Car financing or leasing

- Insurance risk assessments (in some provinces)

A higher credit score can lead to better interest rates, larger borrowing limits, and lower deposits. A lower score can result in higher costs—or being declined entirely.

Typical Credit Score Ranges in Canada

- 300–559: Poor

- 560–659: Fair

- 660–724: Good

- 725–759: Very Good

- 760–900: Excellent

Ways to Start Building Credit

You can start building a credit score in Canada by using credit regularly and responsibly. A common first step is applying for a starter / newcomer credit card, or you can utilize the Compass Credit Union Credit Builder Program. Details about this program are as follows:

COMPASS CREDIT UNION CREDIT BUILDER PROGRAM

- Cash secured loans - with terms between 12 and 60 months

- No application fee (As part of the Welcome to Canada Bundle)

- The interest rate on the loan is set at Compass Credit Union Prime

- The Cash used to secure the loan is held in a Term Deposit so it can earn interest

This program is a great way to build a credit history risk free. It is especially helpful for people who may not want a credit card or who are unable to acquire one. You can also set up automatic payments so that your payments are never late. It’s as easy as set it and forget it!

For more information, or to apply for our Credit Builder Program, speak with one of our lending specialists:

What Positively Impacts Your Credit Score

1. Paying Bills On Time

This is the most important factor.

- Credit cards

- Loans

- Lines of credit

- Utilities or phone accounts (if reported)

Even one missed payment can affect your score for several years.

2. Keeping Credit Card Balances Low

Your credit utilization matters—this is how much of your available credit you’re using.

- Using less than 30% of your credit limit is recommended

- Lower usage generally improves your score

3. Having a Consistent Credit History

Length of credit history helps show stability.

- Older accounts with good payment history are beneficial

- Keeping long‑standing accounts open can help your score

4. Having a Mix of Credit

A combination of different types of credit can be positive, such as:

- Credit cards

- Installment loans (car loans, mortgages)

- Lines of credit

What Negatively Impacts Your Credit Score

1. Late or Missed Payments

- Payments more than 30 days late usually affect your score

- The impact can last 6–7 years

2. High Credit Utilization

- Consistently using most of your available credit—even if you pay it off—can lower your score

3. Applying for Too Much Credit at Once

Each credit application creates a hard inquiry.

- Multiple hard checks in a short time can signal financial stress

- This can temporarily lower your score

4. Accounts in Collections or Defaults

- Unpaid debts sent to collection agencies severely damage credit

- Bankruptcies and consumer proposals also have long-lasting effects

5. Closing Old Credit Accounts

- Closing older accounts can shorten your credit history and reduce available credit, which may lower your score

Important Things You Should Know

- Credit history does not transfer from other countries

- Lenders can require at least 2 years of credit history for large loans and mortgages, so it is important to start building credit as soon as possible.

- Newcomers often start with no credit score, not a bad one

- Building credit requires using it responsibly over time

Many Canadian financial institutions, including credit unions, offer newcomer credit cards and credit‑building programs to help get started.

In Summary

A Canadian credit score reflects how well you manage borrowed money over time. It plays a key role in accessing financial services, housing, and even utilities. The strongest credit scores are built by:

- Paying on time

- Keeping balances low

- Using credit regularly but responsibly

- Maintaining long-term, positive credit habits

Opening an Account in Canada

Opening a banking account is one of the first and most important steps when settling in Canada. A Canadian banking account allows you to receive paycheques, pay bills, save money, and begin building a financial history. Understanding how banking works will help you manage your money with confidence.

To open an account you typically need:

- Government‑issued identification, such as a drivers license, passport or Permanent Resident (PR) card

- Your Social Insurance Number (SIN)

- Proof of a Canadian address, such as a utility bill or rental agreement with your name and address

Even if you are new to Canada and have little or no credit history, you have the right to open a basic personal bank account. Banks cannot refuse you solely because you are new or unemployed, as long as you provide proper identification.

Types of Banking Accounts

1. Chequing Account

A chequing account is used for everyday banking. This includes:

- Receiving your paycheque

- Paying rent and utility bills

- Making debit card purchases

- Sending and receiving electronic transfers

Most chequing accounts charge a monthly fee, although some newcomer packages or student accounts offer reduced or no fees for a limited time.

2. Savings Account

A savings account is designed to help you save money and earn interest.

Key features include:

- Interest earned on your balance

- Ideal for emergency funds or short‑term goals

Savings accounts are not meant for daily spending, but they help your money grow safely.

Canadian Coins & Their Value

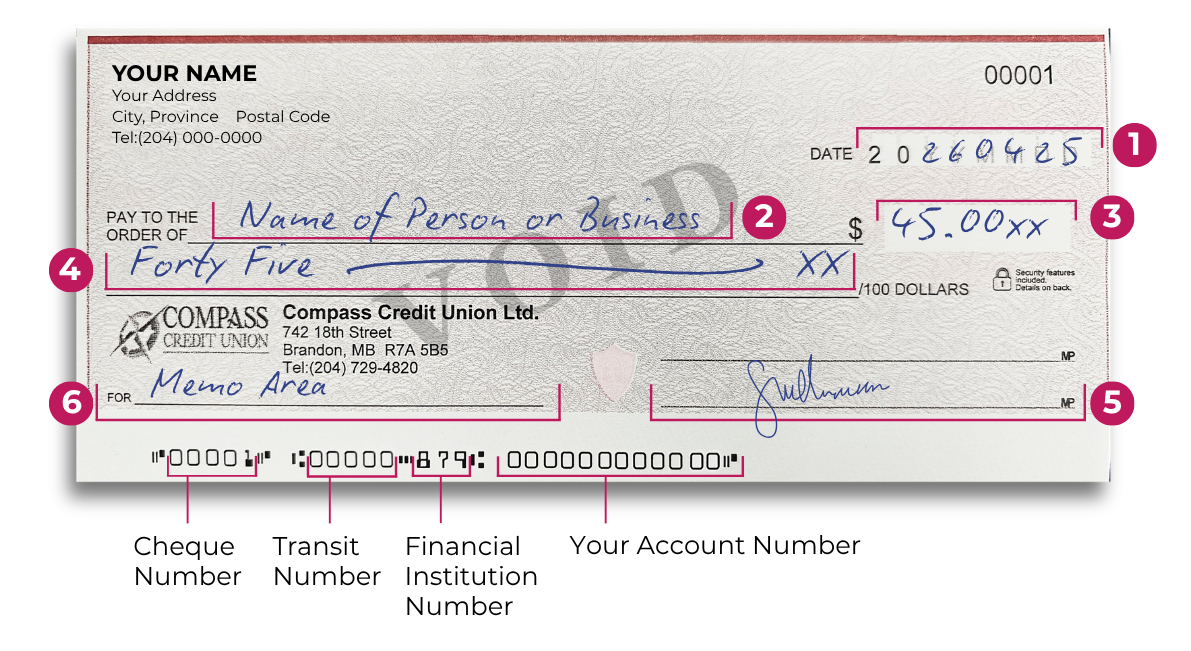

All About Cheques

Even though less common, cheques are still used.

Steps to Write a Cheque:

(click on the number to read each step)

1. Write the date

Marker 22. Write the payee name

Marker 33. Write the amount in numbers (Security Tip: Add “XX” after the final number)

Marker 44. Write the amount in words (Security Tip: Draw a line to the end of the row and add “XX”)

Marker 55. Sign the cheque

Marker 66. Optional: You can use the memo area to mention what the cheque is for.

When a cheque is written, it does not come out of your account immediately. The time it takes to transfer funds between financial institutions is called the holding period. Because of this delay, it’s important to remember that the money will still be withdrawn later. Spending those funds too soon may cause the cheque to be returned due to insufficient funds. This is called a “Bounced Cheque” and can incur an insufficient funds charge on your account.

If you deposit a cheque, you may see the funds appear in your account before the cheque has fully cleared the writer’s bank. While your financial institution may allow early access to some or all of the money, you are responsible for repaying it if the cheque is later rejected.

Keeping track of your chequing account balance may seem outdated, but it is still a helpful way to manage hold periods. Traditional chequebook registers that come with cheques are one option, while spreadsheets or mobile budgeting apps offer more modern alternatives.

Maintaining an accurate transaction record can also help detect fraud or banking mistakes. Comparing your records with your monthly bank statement gives you an extra layer of protection. Recording debit purchases, ATM withdrawals, online payments, and direct deposits turns your register into an effective budgeting tool.

Financial Institutions

Canada has a stable, highly regulated banking system. Most people use:

- Credit Unions (member-owned institutions, often local)

- Banks

- Online financial services

What is a Credit Union?

A credit union is a financial institution that provides many of the same services as a bank—such as savings accounts, chequing accounts, loans, credit cards, and online banking—but operates in a fundamentally different way.

Member-Owned, Community-Driven

- The biggest difference between a credit union and a traditional bank is who owns it.

- Credit unions are owned by their members (the people who use their services).

- When you open an account at a credit union, you become a member-owner, not just a customer.

- Profits are not paid to shareholders—instead, they are reinvested to benefit members through better rates, lower fees, and improved services.

Built on the Idea of Community

Credit unions are typically formed to serve a specific community or group, such as:

- People who live or work in a certain area

- Employees of specific organizations

- Members of certain associations or communities

Because of this, credit unions tend to have a strong focus on:

- Local decision-making

- Supporting community initiatives

- Building long-term relationships with members

Democratic and Member-Focused

Credit unions operate on a democratic model:

- Each member gets one vote, no matter how much money they have in the credit union.

- Members can vote for the board of directors and have a say in major decisions.

- Leadership is focused on what’s best for the membership as a whole—not maximizing profits.

Financial Services with Member Benefits

While credit unions offer most of the same services as banks, their structure often allows them to provide:

- Competitive interest rates for loans and deposits

- Competitive service fees

- More flexible lending decisions, especially for first-time borrowers

Safe and Secure

Credit unions are just as safe as banks. In Manitoba, deposits are 100% protected by provincial deposit insurance, which safeguards your money in the event of a financial institution failure.

Values-Driven Banking

Many credit unions emphasize values such as:

- Financial education

- Ethical and responsible lending

- Supporting local businesses

- Helping members improve financial well-being

Taxes in Canada

Filing taxes in Canada may feel overwhelming at first, but it is an important responsibility—and it also helps you access valuable government benefits. Whether you are new to Canada or filing for the first time, understanding the basics can make the process much easier.

Who Must File Taxes?

Most people living in Canada are required to file an income tax return each year, even if they earned little or no income. Filing is especially important because many government benefits are available only if you submit a tax return.

You should file taxes if you:

- Worked or earned income in Canada

- Are a resident of Canada for tax purposes

- Want to receive benefits and credits such as GST/HST credits or child benefits

Even if you do not owe taxes, filing ensures the government has up-to-date information about your income and household.

Key Tax Concepts to Know

Income Tax

Income tax is based on how much money you earn during the year. Canada uses a progressive tax system, which means:

- Lower income is taxed at a lower rate

- Higher income is taxed at higher rates

Income can come from employment, self-employment, investments, or certain benefits.

Sales Taxes

When you buy goods or services, you usually pay:

- GST (Goods and Services Tax) – a federal tax

- PST (Provincial Sales Tax) – charged by provinces like Manitoba

Some provinces combine these, but Manitoba keeps them separate.

How to File Your Taxes

Filing taxes is a step-by-step process and can be done online or with professional help.

Step 1: Collect Your Documents

Common tax slips include:

- T4 – Employment income from your employer

- T5 – Investment or bank interest income

Step 2: Choose How to File

You can file your taxes by:

- Using online tax software like TurboTax or Wealthsimple Tax

- Hiring an accountant or tax professional

Many software options guide you through the process and submit your return directly to the Canada Revenue Agency (CRA).

Step 3: Submit to the CRA

Once submitted, the CRA reviews your return and issues a Notice of Assessment, showing any refund or balance owing.

Important Tax Deadlines:

Missing deadlines can result in penalties or delays in receiving benefits.

- April 30 – Filing deadline for most individuals

- June 15 – Filing deadline if you are self‑employed

- April 30 – Any taxes owed must still be paid by this date, even if you are self‑employed

Benefits You Get from Filing Taxes

Filing your taxes allows you to receive important benefits, including:

- GST/HST Credit – helps offset sales taxes

- Canada Child Benefit (CCB) – monthly payments for eligible families

- Climate Incentive Payments – rebates to help offset carbon pricing

These benefits are recalculated every year based on your tax return.

Taxes Resources & Information

CRA’s website has a lot of information and education on taxes. You might find this link helpful:

Important Government Programs

In Canada we have several government programs that are important to be aware of:

Canada Pension Plan (CPP)

- Retirement income

Employment Insurance (EI)

- Temporary income if unemployed

Old Age Security (OAS)

- Seniors benefit

Settlement Services

Additional assistance with settlement, resources, and programs, are available at: